Hasenstab on Global Growth: Headwinds or Tailwinds?

By: Michael Hasenstab, Ph.D.

Executive Vice President, Chief Investment Officer

Portfolio Manager

Templeton Global Macro Group*

While some forecasters predict gloomy global growth this year, the contrarian-minded Dr. Michael Hasenstab, chief investment officer, Templeton Global Macro Group (formerly known as Templeton Global Bond Group), has a different view. He aims to counter what he sees as “excessive pessimism” surrounding the global economy and outlines why he believes the recent plunge in oil prices could prove a tailwind, not only for economic growth in the United States, but also in Europe. He also offers his scorecard regarding Japan’s monetary policy experiment dubbed “Abenomics.”

Excessive pessimism characterizes the current view on the global growth outlook, in our view. Many observers see the lowering of global growth forecasts by the World Bank and the International Monetary Fund (IMF) as confirming a loss of global economic momentum. Some of this pessimism also reflects a mistaken interpretation of the reasons behind the recent sharp decline in oil prices, and of its likely consequences. Many analysts and commentators have argued that the plunge in oil prices reflects the slowing down of the global economy, and some believe that the decline in oil prices itself will have a negative impact on global growth, by reducing energy investment and causing deflation in some regions. As for key economic areas, while most observers are more upbeat on the United States, many observers seem to expect a major slowdown in China and to view the eurozone as being on the brink of recession.

However, even the latest IMF forecasts, which have generated so many pessimistic headlines, show the global economy accelerating, not decelerating. The IMF argues that the weakening of global oil demand is due to a loss of momentum concentrated in emerging markets, which have a higher energy intensity than advanced economies. But the slowdown in emerging markets overall has been marginal, and, most importantly, China’s oil demand continued to rise through the end of 2014.

Some of the risk aversion that we have been seeing recently in the markets really dates back to late last year, and we believe a lot of it has to do with a market misread of the decline in oil prices. There are three things that we think the market has misinterpreted.

The first relates to whether the fall in oil prices is due to a decline in demand or a change in supply. If it is due to a decline in demand, we think there would be reason to be bearish about the outlook for risk assets, in line with a slower global growth environment. However, it’s our assessment that the price of oil today is largely a function of change in supply due to political reasons, particularly driven by Saudi Arabia and the Organization of the Petroleum Exporting Countries (OPEC). As a result, we believe investors should think about the changing price of oil as essentially a large global tax cut to the world of oil importers. If we look at most of the major economies—China, the United States, Europe and Japan—they are all large users of oil and, as a result, will likely benefit from lower oil prices. We think the fact that the decline in the price of oil appears predominantly driven by supply factors could actually be a tailwind for the global economy in 2015.

The second has to do with the sequencing of effects. In the United States, for example, the initial reaction to the plunge in oil prices could be a decrease in investment and some loss of jobs in oil-intensive sectors. But those should be shorter-term effects that we believe ultimately should be reversed over the course of the year as resources get redeployed from oil-intensive sectors to other sectors of the economy, and as those de facto tax cuts (lower oil costs) to the US consumer begin to take hold. So by the middle or end of 2015, we expect the effects of these changing dynamics in the oil markets to actually have an aggregate positive impact on the United States, as well as globally, based on similar dynamics. Investment and employment in the energy sector play a much smaller role in the economy than overall personal consumption, which accounts for about 70% of gross domestic product (GDP). We estimate that, on net, lower oil prices should add about 0.7 percentage points to US growth on an annual basis.

China, as the world’s largest importer of oil, will also be an important beneficiary of lower energy prices. This should help further mitigate the current mild and healthy slowdown, so that we expect 2015 growth of about 7%, only marginally slower than last year. Importantly, the quality of investment has improved, albeit at a slower rate. This combined with a growing level of consumption as a contribution to growth puts China on a path toward the long sought after rebalancing. We would also observe that as China’s economy has grown substantially over the past decade, even at a more moderate growth rate its total contribution to global growth will remain larger than that of the United States. If China grows at 7% in 2015, the quantum of demand it produces for world GDP will also be larger than in the prior year.

The third dynamic has to do with inflation. Oil is a big input within headline inflation statistics, so obviously, a 50% fall in the price of oil would be reflected in the rapid decline in headline inflation. However, we see this as more temporary in nature. Unless the price of oil falls another 50% from where it is currently, these effects will likely roll off by the end of this year, and the underlying dynamics of improving demand should actually start to reverse some of the inflation numbers. So, we think the market may be getting lulled into a sense of comfort as headline inflation numbers have been coming down. We don’t expect that to last, and believe investors should be very wary of taking too much interest-rate exposure in this type of environment.

US Economic Growth and Monetary Policy: Will the Fed Pull the Trigger on Rates?

We think the Federal Reserve (Fed) will likely start normalizing interest rates in 2015. And while it’s true that there’s been a lot of focus on the fact that wage rates are not rising as much as the Fed would like them to, it’s important not to look just at the rate of increase in wages, but also to look at the aggregate labor bill. To do that, you need to look not just at the wage rate, but at the number of people working and the hours they are working. If you look at that number for aggregated labor earnings, it is significantly higher than it was prior to the 2007–2009 financial crisis. Looking at real disposable income, there are also a number of metrics that have all significantly exceeded their pre-crisis levels. There certainly have been some dislocations in the labor market, but we don’t think the excessively easy interest rates that the Fed has been running for years are still justified today.

Europe: Headwinds and Tailwinds

Europe certainly faces a number of headwinds, including large structural impediments in the labor and product markets, and a lack of coordination between a number of economies in the region. In our view, those impediments are unlikely to change significantly in 2015, but they are all largely baked into market expectations and predictions of 2015 growth.

However, there are some important tailwinds that we think the market may be ignoring, which could result in some upside surprises when it comes to Europe’s outlook. The first and most meaningful is the euro currency depreciation. We expect it to continue to depreciate as the European Central Bank (ECB) embarks on a very aggressive quantitative easing (QE) program. This currency depreciation should boost exports, and we expect it to have a meaningful inflow, or feed-through, into European growth. Strong consumer demand from the United States should provide an additional tailwind in boosting European exports.

Another tailwind for Europe is the aforementioned decline in oil prices. As an oil importer, the eurozone should benefit in aggregate from lower oil prices. The IMF estimates that the incremental impact on euro area growth from such a reduction in oil prices could be as much as 0.5%.1 The ECB has a more conservative forecast, but we think the key factor remains that the decline in oil prices will support growth—adding to the potential for an upside surprise to expectations of the region remaining mired in stagnation in the year ahead. These factors put us squarely at odds with currently perceived wisdom that sees the eurozone as the source of global growth fears, and thus in part the cause of the collapse in oil prices due to an impending decline in demand.

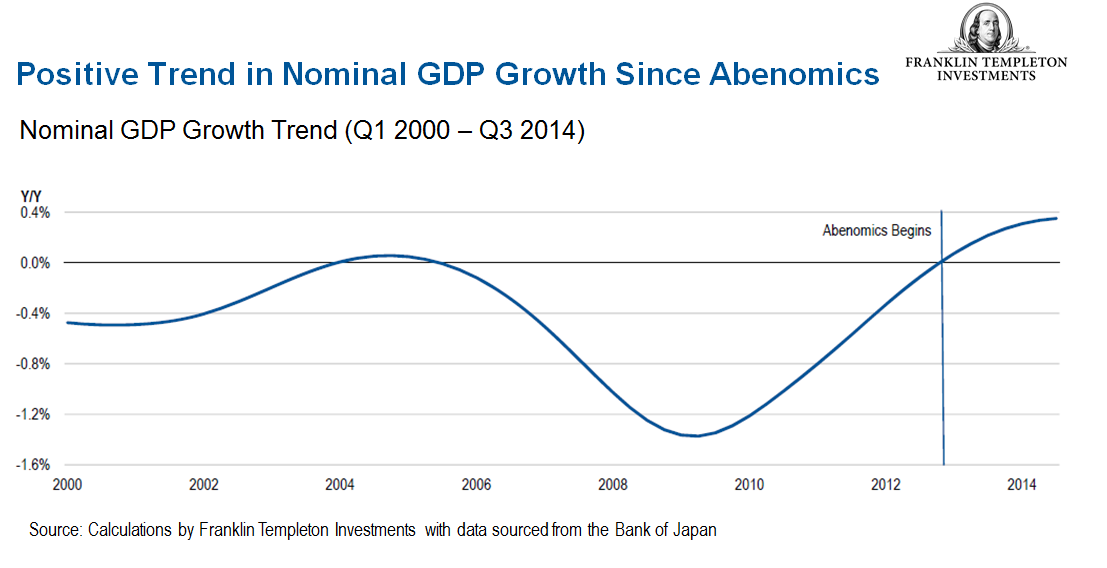

Abenomics: A Report Card for Japan

Japanese GDP growth should rebound to over 1% this year,2 above potential, thanks to the expansionary macroeconomic policy and favorable external environment. The IMF estimates that a 50% reduction in oil prices would likely raise Japan’s GDP by up to about 0.5% in 2015.3 A certain degree of uncertainty accompanies this estimate given the clear increase in oil imports after the Fukushima earthquake in 2011. The positive growth impact will likely be gradual and materialize with some quarters’ lags.

The question remains whether this begins a temporary or permanent exit from Japan’s cycle of deflation, rising debt and declining growth. The answer will depend on whether Prime Minister Shinzō Abe’s government manages to make equally decisive progress on other key reforms.

Abstracting from the impact of oil prices, we recognize that the efficacy of Abenomics, the Japanese macro policy experiment in place since early 2013, generates some skepticism. We believe Abenomics—the name given to Prime Minister Shinzō Abe’s ambitious, three-pronged policy to jump-start growth and inflation in Japan that includes QE—needs to be broken down into two components: the short term and the medium to longer term. In the short term, we think Abenomics has been successful. The risk of deflation in Japan has decreased massively; some observers estimate that the risk of deflation in Japan is currently lower than for most other economies globally. Amid a lowering of real interest rates, Abenomics has also been successful in boosting asset prices and depreciating the yen. We see these as signs of success for the first phase of Abenomics.

We think what will determine whether Abenomics is ultimately successful over several years will have to do with structural reform. We need to see labor market reform and product market reform in Japan, as well as increases in the tax regime, in order to make Japan’s debt sustainable, in our view. So we think the first phase has been successful, and Abe has been a very astute political tactician. He sequenced his reforms to maintain his political popularity, which gives him the legitimacy to undertake the type of reforms that will not be very popular going forward. We believe the sequencing from a political standpoint has been very successful, and Abe deserves a lot of credit for that. It remains to be seen if he can use that political legitimacy to execute the longer-term and very difficult reforms that are necessary to get Japan’s debt-to-GDP on a more sustainable path.

In summary, over the past few months, global financial markets have been broadly influenced by the pickup in growth in the United States, the economic stabilization in China, and the abundance of global liquidity from the Bank of Japan and the ECB—which should remain focal points in 2015.

The core of our strategy for 2015 continues to be positioning to navigate an anticipated rising-rate environment in the United States. We have continued to prefer short portfolio duration while aiming for a negative correlation with US Treasury returns. We also actively seek opportunities that can offer positive real yields without taking undue interest rate risk. We maintain our conviction in a strengthening US dollar against the yen and euro and continue to look for investment value in the currency and bond markets of select emerging-market economies.

* Dr. Hasenstab and his team manage Templeton’s global bond strategies including unconstrained fixed income, currency and global macro. This economic team, trained in some of the leading universities in the world, integrates global macroeconomic analysis with in-depth country research to help identify long-term imbalances that translate to investment opportunities.

Dr. Hasenstab’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

What Are the Risks?

All investments involve risk, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Currency rates may fluctuate significantly over short periods of time, and can reduce returns. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size and lesser liquidity. Investments in lower-rated bonds include higher risk of default and loss of principal. Changes in interest rates will affect the value of a portfolio and its share price and yield. Bond prices generally move in the opposite direction of interest rates. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value.

- Source: International Monetary Fund.

- Source: Bank of Japan.

- Source: International Monetary Fund.

Related Articles

Charles Brandes – Top bets are outside North America

Value investor Charles Brandes finds bargains in Japan and the emerging markets Despite the recent strengthening of U.S. stock markets,

Malaysia’s 2020 Budget: A Delicate Balancing Act

Malaysia’s newly unveiled 2020 budget displays a commitment to sustainable long-term growth, according to Sukumar Rajah and Hanifah Hashim. Here,

Income-starved investors finding higher income in emerging market bonds

With interest rates at record lows in North America, investors seeking higher fixed income returns are heading in droves to