Malaysia and Islamic Finance in Emerging Markets

The world of Islamic finance and investing represents an exciting world of opportunities for Muslims all over the world, and one we think should likely continue to grow. I recently had the pleasure of attending the Global International Islamic Finance Forum (GIFF) in Malaysia and had the opportunity to share our team’s views as well as exchange information on the future of Islamic finance in emerging markets. More than a thousand participants from around the world attended this year’s GIFF in Malaysia, which I think is testament to the growth of Islamic finance.

Many investors outside the Muslim world might not know much about Islamic finance, but recognition and interest in it has been growing globally. Bank of Malaysia Governor Datuk Muhammad bin Ibrahim spoke at the GIFF and reported that by 2020, total assets in global Islamic finance are expected to reach more than US $3 trillion.1 He also said that in at least 10 jurisdictions, Islamic banking today represents more than 20% of total banking assets, and in many countries, Islamic banking services are offered in tandem with traditional types of financial services and products.2

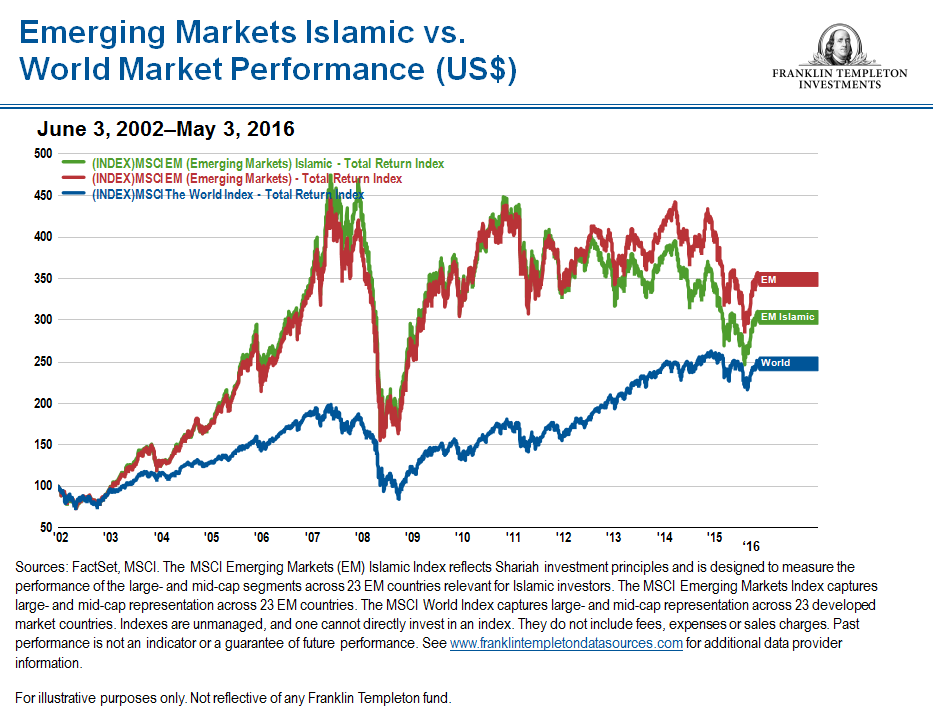

For those who are not familiar with Islamic finance, it encompasses both equity and credit-based investments (called sukuk) that are compliant with Islamic (Shariah) law. The goal is the same as with other types of investments: to produce a favorable return and/or generate income. The difference is that Islamic investments must adhere to various tenets, including the prohibition of the payment of interest (so-called “riba”) as well as certain forbidden activities and products including alcohol, armaments and a number of foodstuffs and food-related activities. The interpretation of what is Shariah-compliant and what is not can be complex, requiring the active involvement of Islamic scholars (who may not always agree). This can add a layer of complexity for investors. If the main business of a company is not deemed compliant with Shariah law, a portfolio manager cannot purchase, hold or sell its shares. Of course, the desired goal or purpose of any investment is to make money for those who invest in it. So, I think it is worth a look at how these types of investments have performed versus emerging market equities more broadly and versus global equities in developed markets more broadly. You can see in the chart below how the MSCI Islamic Total Return Index has largely mirrored the performance of the MSCI Emerging Markets Total Return Index since 2002 with some slight variations, while generally outperforming the MSCI World Index.3 Of course, some countries’ equity markets have performed better or worse than others. We would note that Islamic investment indexes in Indonesia, Turkey and Malaysia have seen some periods of volatility but have generally outperformed many other countries in this category since 2002.4

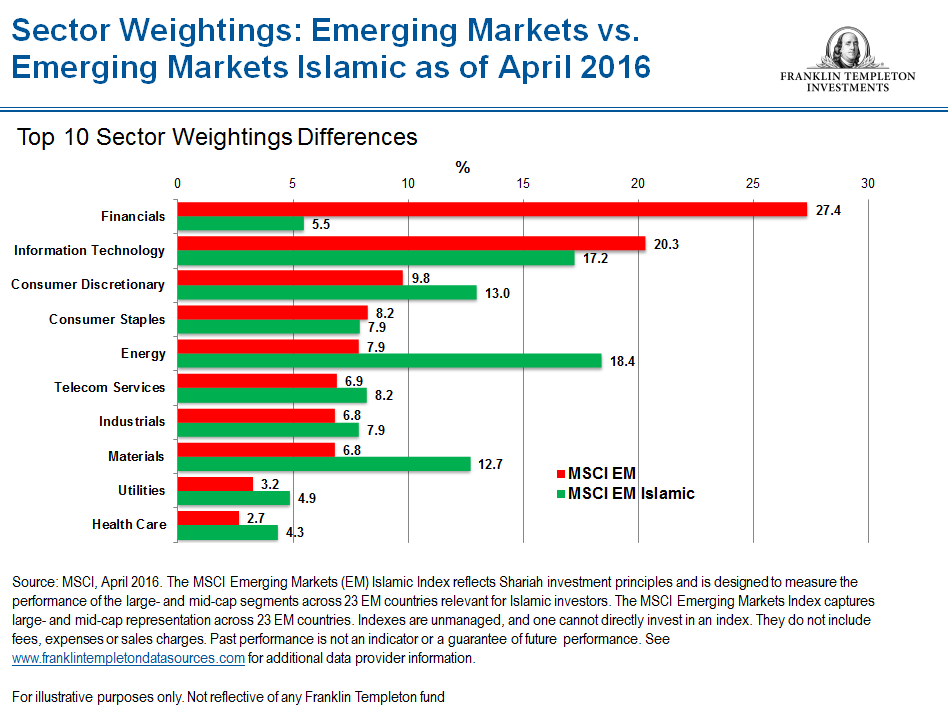

If you look at the sector weightings of the MSCI Emerging Markets Islamic Index versus the more general MSCI Emerging Markets Index, you will see significant differences. For example, financials is much smaller in the Islamic Index, while consumer discretionary and energy are much higher for the Islamic index. Country weightings also differ between the indexes.

Economic Growth in the Muslim World

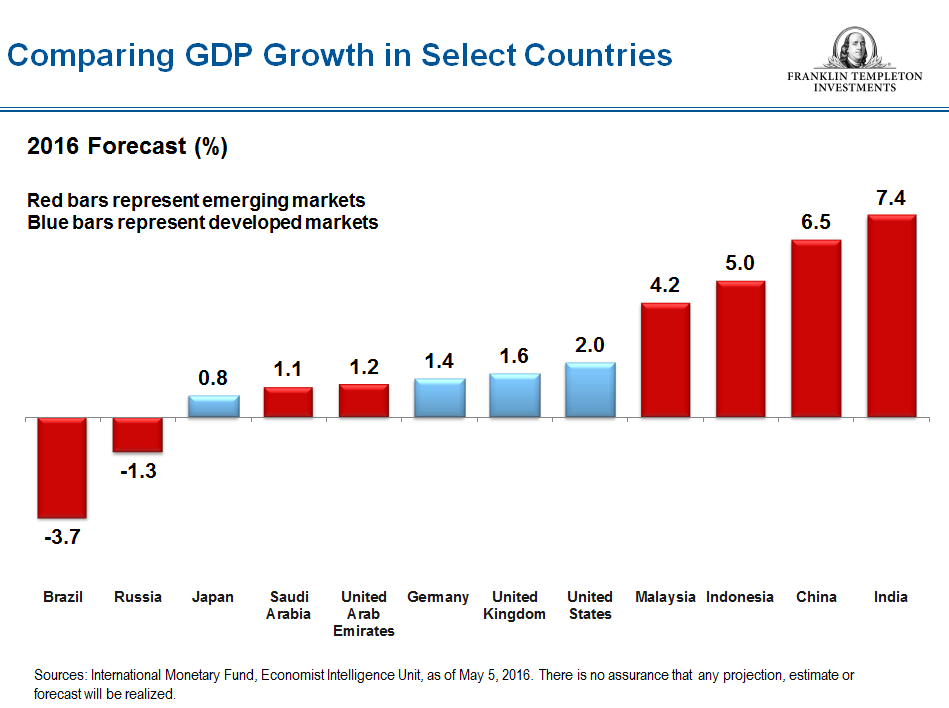

Muslim populations have been growing worldwide, and economies in Muslim countries have similarly been growing. In 1987, Muslim-majority countries represented about 4% of global gross domestic product (GDP); as of December 2015, they represented about 8% of global GDP.5 We believe that percentage will continue to grow. We also have observed that GDP growth has been higher in emerging markets generally (including many Muslim countries) than in developed markets over the past two decades.

Many Westerners associate countries in the Middle East with the Muslim world, but some countries in Africa and Asia also have large Muslim populations and good potential growth trends, Indonesia being the most populous individual Muslim country. In the charts below, you can see the estimated growth and growth forecasts for Muslim-majority countries as well as select emerging markets versus select developed markets.

Malaysia: Islamic Finance Hub

At the GIFF, Malaysia’s central bank governor discussed Malaysia’s role as a global leader in Islamic finance, which operates alongside conventional financial markets. Malaysia has been a pioneer in Islamic finance, and the central bank’s efforts to develop Islamic finance span more than three decades. In 2001, the Securities Commission Malaysia provided a framework for establishing the country as a leader in Islamic finance as part of its first 10-year “Capital Market Master Plan.” In 2006, the Malaysia International Islamic Financial Centre (MIFC) was launched to help further its goal of becoming an international Islamic financial hub—which I think clearly has been achieved!

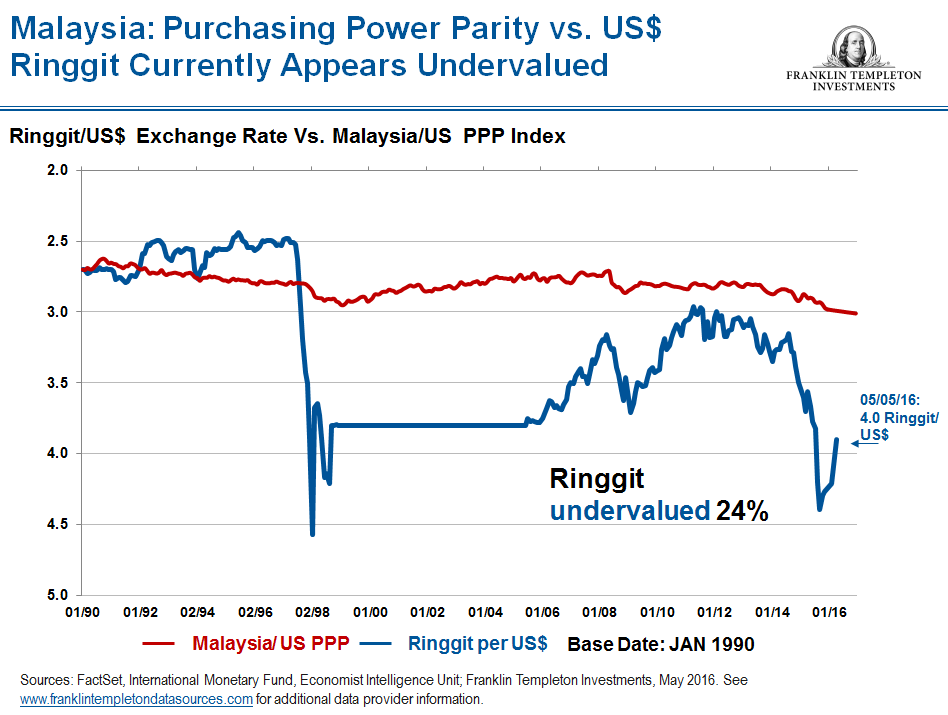

Malaysia’s equity market has experienced weakness this year, along with its currency, which fell to its lowest level versus the US dollar since the mid–late 1990s, at a time Asia was experiencing financial crisis. We had to ask ourselves: Was it really that bad in the country—was this year’s selloff justified? There are many ways to determine currency valuations, but we use purchasing power parity to help determine whether a currency is overvalued or undervalued. This measures inflation in one country versus inflation in the United States. So, for example, if inflation in Malaysia, China or any other country is higher than inflation in the United States, those currencies should naturally decline versus the dollar. Based on this measure, we currently see the currencies of both China and Malaysia, as well as the currencies of Indonesia, Thailand and Saudi Arabia, appearing to be undervalued. We also see equities in emerging markets generally undervalued based on measures such as price/earnings and price/book ratios.

Related Articles

Southeast Asia’s Internet Economy: On a Fast Track

Conditions have been ripe for Southeast Asia’s e-transformation, and COVID-19 has acted as an accelerant, according to Claus Born and Yi

A Spiritual Journey in Thailand

Thus far Thailand’s stock market has been relatively resilient amid bouts of global market volatility following the United Kingdom’s recent

Why It’s Not Time to Squeeze the Brakes on Indian Equities

As Indian equities have come off the peaks from the start of the year, some emerging-market investors may be feeling