Once Forbidden Frontiers

Investing in frontier markets can come with a higher degree of volatility than more established markets, but to my team and me, they offer exciting potential. Some of yesterday’s small, agrarian economies have transformed themselves into global powers today—China being the most impressive example. China represents the second-largest economy in the world today, depending on how you crunch the numbers, and it has been incredible to see the changes taking place there in my lifetime. It got me thinking about economies that were viewed as largely untouchable or risky for investors and travelers even just a few years ago, but that today are being discussed as interesting potential destinations for both.

Here are some examples from recent history of countries that were shunned or out of favor in the international community at large, but have undergone big transformations. This includes some emerging and frontier markets that are currently of great interest to us, and countries we are not yet investing in, but that are opening up to investors.

China

In 1950, trade between the United States and China was roughly US$200 million annually when China became subject to an embargo that lasted 21 years, ending in 1971.1 Today, trade between China and the United States adds up to more than US$500 billion, making China the United States’ second-largest trading partner.2 China has undergone a huge growth spurt over the past three decades and has transformed its economy. For emerging markets investors, China is a destination that certainly can’t be ignored and remains an engine of growth for the world. Even if market watchers have to get used to a “new normal” of slightly slower gross domestic product (GDP) growth than in past years, we think the 7.4% growth rate China reported in 2014,3 and the target of around 7% in 2015 Chinese premier Li Keqiang gave at the National People’s Congress in early March still looks impressive, given the size of China’s economy, and is not something that concerns us.

Japan

An adversary to the West in World War II, Japan is an example of a market that moved rapidly from frontier to emerging to developed market status and is now considered one of the strongest allies of both the United States and Europe. Japan’s rise to economic strength has been well-documented as one of the biggest post-WWII achievements and its high-quality, high-tech goods have permeated nearly every corner of the globe. Since its boom times of the 1980s, Japan’s economy might be stagnating, but it still holds plenty of sway in the world’s economy. Its government has been working to increase consumption and jump-start growth through an ambitious, three-pronged fiscal and monetary approach. In our view, the quantitative easing regime the Bank of Japan began in 2013 that continues today should help support global liquidity and trickle down to emerging markets in the region.

South Africa

Apartheid, a system of legalized discrimination dating back to the 1950s, cast a shadow on South Africa in the eyes of the international community for many years. In addition to United Nations sanctions, the US Congress passed the Comprehensive Anti-Apartheid Act in 1986, resulting in the withdrawal of many large multinational companies from South Africa. The end of apartheid in South Africa in 1994 opened the door again to wider investment in the country, but since then, its economy has been struggling to reach its full potential for a variety of reasons.

South African stocks have started 2015 on a solid note, aided by the recent drop in oil prices. In particular, retail businesses (particularly clothing and food) seem to be benefiting from the potential boost to domestic consumption from lower fuel prices. While South Africa has been struggling with an electricity crisis that could stunt GDP growth this year, we continue to believe that attractive long-term investment opportunities exist across a range of South African markets and sectors.

With the government’s focus on redistribution of wealth and extensive social grants, companies that provide goods and services to consumers at the low end of the income scale have benefited tremendously and, in our view, should continue to do so. Also, many South African-based companies that generate a substantial portion of their income from operations and investments in other markets have benefited from a weakening of the South African rand relative to the US dollar and other major currencies. The real estate sector has been stable with price growth in recent years, fueled by demand that substantially outstrips supply, especially at the entry level. In this regard, the financial sector plays a key role, with banks taking a fairly conservative approach to both asset-backed and non-asset backed lending activities. Moreover, a number of South African companies are investing on the rest of the African continent across a variety of industries, including infrastructure, retail, financial services and telecommunication.

Here are some examples of frontier markets that were out of favor, but are transforming and opening up to wider foreign investment. These are just a few of the markets in which we are investing, or watching for potential future opportunities.

Vietnam

Since the end of what’s known as “the Vietnam War” in the United States and “the American War” in Vietnam, the country has seen some huge changes. Vietnam’s rise hasn’t been as powerful or fast as Japan’s post-WWII experience but a construction boom has been underway. In 2010, Vietnam got its first skyscraper, the striking Bitexco Financial Tower, which stands as a beacon in Ho Chi Minh City. An even taller building is currently under construction in the city, expected to rise to about 350 meters and contain a luxury hotel, apartments, shopping and what is said to be Southeast Asia’s highest restaurant and bar. Franklin Templeton has an office in Ho Chi Minh City, and it’s been exciting to visit the city and see the changes taking place there and around the country.

The middle class has been growing in Vietnam and people have also been trading in bicycles for motorcycles, scooters and automobiles. To help alleviate the traffic on busy city streets, Vietnam’s first-ever subway system has been under construction with the help of foreign investment from Japan, France and China.

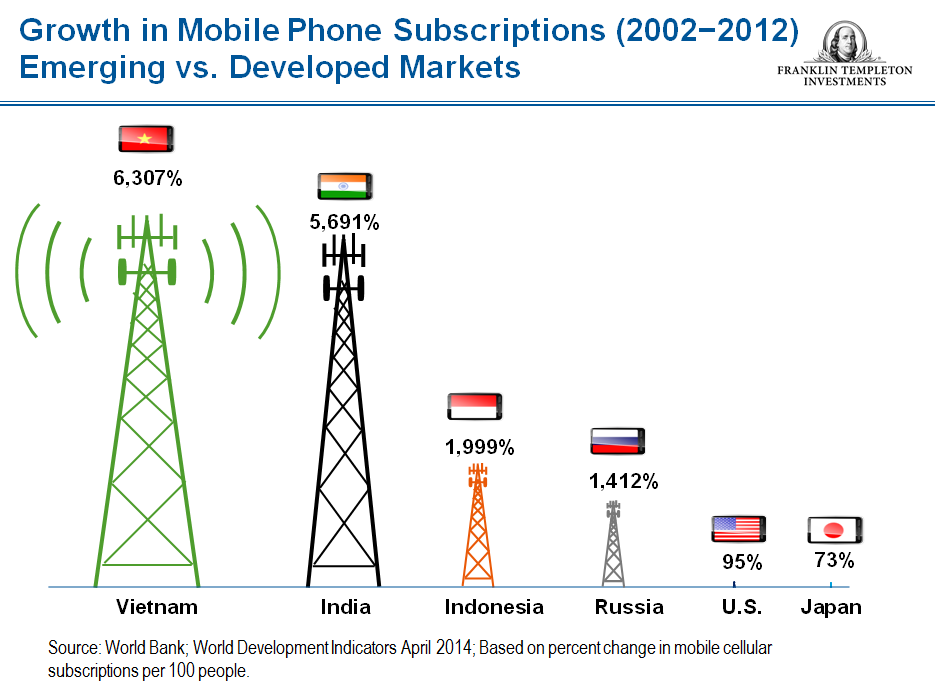

The chart below shows how Vietnam’s people have been eager to have access to new technology, with growth in mobile phone subscription rates topping even India and the United States during 2002–2012.

While it is clear there has been progress, Vietnam’s transformation has been slower than we’d like. The war was so traumatic and the people remain a bit sensitive about foreign dominance, which has hindered the acceptance of foreign investment. The Vietnamese seem to be gradually overcoming these reservations because of the positive developments they see to the north in China, and we have recently seen more movement in allowing greater foreign investment. Vietnam’s stock market is not very liquid, and it is considered a frontier market; but Vietnam has had a fast-growing economy, and we have found good companies there, including some that are state-owned.

Myanmar

I had the pleasure of visiting Myanmar earlier this year, and it’s a perfect example of what we view as “the next frontier” of untapped markets in which we aren’t yet investing but are closely watching. It’s truly a wonderful place that has seen a big change in policy and global perceptions. My most recent visit included a trip to Mandalay, an incredible city with its royal palace still intact. The city remains in a time warp but 640 kilometers to the south, the country’s largest city and former capital, Yangon has skyscrapers and development. Growth has also been robust, with GDP growth of more than 8% in 2013 and 2014 and expected at a similar pace in 2015.4 However, Myanmar’s capital markets have a long way to go before we can consider investing there in a meaningful way. Elections coming up in November could have a big impact on acceptance by the United States and other countries that have had embargoes and other constraints to doing business there. If Myanmar can successfully hold an election that’s considered to be fair, we might see more constraints loosened.

During our visit, my team and I met with officials who are planning a stock exchange, but it will take some time to develop the necessary financial system infrastructure. Implementation of foreign investment will take time; in order to invest, we need custodial banks and so on.

To do business effectively in a country, we believe it’s important to understand the culture and the people, including traveling there and talking with ordinary citizens as well as government officials and business leaders. Myanmar is steeped in history and is deeply religious; gold-covered pagodas can be spotted in nearly every city, and in the countryside, you can sense the deeply embedded spirituality in the culture.

Cuba

Cuba is another country that we are not yet able to invest in, but are watching closely. There has been a lot of excitement recently about what appears to be a new chapter in Cuba-US relations, including the possible restoration of diplomatic ties between the countries and the end to decades of US sanctions. The US State Department has conveyed that the United States aims to lift restrictions on travel, commerce and financial activities with Cuba. However, with a Republican-controlled Congress and a strong anti-Castro Cuban diaspora still holding some influence in the United States, it seems unlikely that rapid progress will be made unless there are more signs of democratic reforms in Cuba. Nevertheless, it seems obvious there will be some opportunities for airlines to increase flights to the island following relaxed travel rules—and we’ve already heard that message from a few US carriers eager to service or expand existing charter services to Cuba. US banks could also benefit since US tourists visiting the island will be allowed to use credit and debit cards issued by their banks, and US bank accounts of Cuban citizens living on the island will be unlocked. Remittances from the United States to Cuba are being raised from a maximum of US$2,000 to US$8,000 annually, but unless the 1962 embargo instituted by US President John F. Kennedy is lifted, foreign investment from the United States into Cuba will remain severely restricted.

In my view, the impact on US firms of the new relationship with Cuba will likely be limited, at least in the short to medium term, but the gains for non-US firms could be substantial. I think Cuba’s ability to access the US market could make investing in export-oriented Cuban enterprises more attractive. If the embargo were to be lifted, then Cuban companies that escaped to the United States after the revolution could return and relocate there. The Castro government’s tight grip on the economy remains an additional barrier to wider investment, but there are some signs it could loosen, and food could be the first item of trade to be liberalized in Cuba. A US Agriculture Commission for Cuba including about 30 US companies and food-related groups headed by an executive of a US food giant has been lobbying the US Congress to lift the trade embargo with Cuba and ease trade sanctions. Despite the obstacles, we think the long-term opportunities for potential investment in Cuba look enormous.

Frontier Markets General Outlook

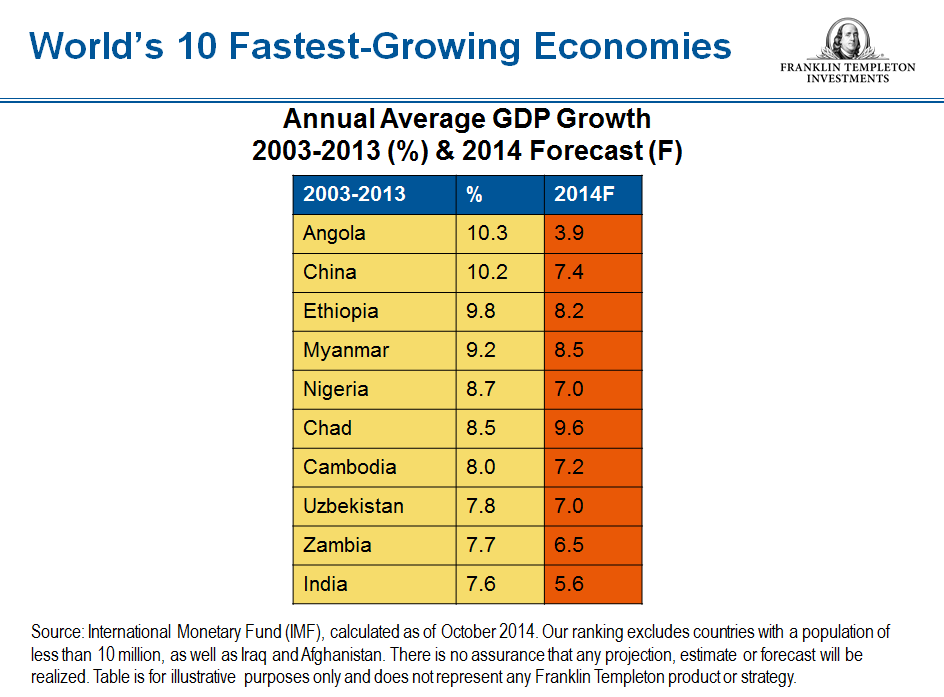

These are just a few frontier markets we are watching—there are many more we are also excited about. Looking long term, we believe the structural reasons behind frontier investing in general remain generally solid, including good potential growth rates in many frontier economies, strong domestic and capital markets growth, technology transfer, demographic advantages and generally low sovereign and private indebtedness. Of the 10 countries estimated by the International Monetary Fund to have achieved the fastest economic growth between 2003 and 2013, eight were frontier markets, with China and India being the other two (see chart below). The underlying growth profile can be particularly attractive in frontier markets, as they tend to be more exposed to their domestic economies—many of which are developing rapidly—as opposed to the global economy, which is growing at a slower pace. Furthermore, technology leapfrogging and partnerships between emerging markets that are able to supply capital and technology (such as China), and frontier markets with low labor cost structures, could be particularly potent sources of growth.

In the current environment, a number of countries are undergoing positive developments while headwinds remain for others. Headlines of conflict and tension in some emerging and frontier markets continue to affect overall investor sentiment. At the same time, the improving macro environment and lower political risk have benefited individual economies (Sri Lanka and Bangladesh being two examples). In recent days, major world powers have been discussing a United Nations Security Council resolution to lift sanctions against Iran. Meanwhile, planned economic reforms and a new International Monetary Fund loan program could further promote Pakistan as an investment destination.

While we don’t know what the future will bring, this demonstrates to us how important active management—including on-the-ground research and a bottom-up stock selection process—is when it comes to investing in emerging and frontier markets.

Mark Mobius’s comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including possible loss of principal. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets.

- Source: Washington Post, June 11, 1971, “US Ends Ban on China Trade.”

- Source: US Census Bureau, 2013 data.

- Source: National Bureau of Statistics of China, January 2015. There is no assurance that any forecast will be realized.

- Source: IMF World Economic Outlook database, October 2014. There is no assurance that any forecast will be realized.

Related Articles

Is African economic growth finally ready to take off?

Long seen as “too risky,” African economic growth is moving forward at a remarkable pace Africa has experienced a sea

Why the MENA Region Appears to be on Firmer Footing

As Middle East and North Africa (MENA) economies adapt to the reality of sustained lower oil prices, Dino Kronfol, chief

The developing potential of Middle East markets

Middle East markets have the potential to become the newest emerging-market frontier for investors. The region’s problems garner attention, but beneath