Chinese New Year: How Investors Might Navigate Markets in the Year of the Ox

As the upcoming Chinese New Year ushers in the Year of the Ox, could it be the year Asian economies power ahead? Franklin Templeton Investment Solutions’ Stephen Tong, Franklin Templeton Emerging Markets Equity’s Michael Lai and Western Asset Management’s Desmond Soon think so.

Ahead of the new lunar year, they weigh in on how investors might navigate Asian markets with the characteristics of the Chinese zodiac’s ox in mind, traditionally associated with patience, diligence and persistence.

The ox is the second animal in the 12-year cycle of the Chinese zodiac. Its arrival on February 12, 2021, a year after COVID-19 came to light across the world, comes at a time where there is elevated uncertainty among investors over the pace of global growth. While a full global recovery is unlikely, we think there are some potential bright spots in Asia.

Transition from Crisis Measures to Supporting Recovery Shines New Light on Asset Allocations

Stephen Tong

The global pandemic has pushed the global economy into a deep recession, though the market has widely factored in the expectation of a sharp economic rebound. There’s a huge divergence over the pace of global growth. The recovery path will likely be uneven, especially between the East and the West. We believe Asia is on a better path of recovery and that China in particular should be on track for a strong rebound and on-trend growth over the mid to long term. This is a reflection of the ox’s diligent role in Chinese agriculture.

Central banks around the globe remain accommodative and maintain a “whatever it takes” attitude to keep interest rates low. We’ve been impressed at the targeted stimulus measures, particularly in China. The People’s Bank of China’s (PBOC’s) prudent response to the effects of COVID-19 last year freed up billions in reserve requirements for banks, which in turn funded loans to help the worst-hit companies from the virus outbreak.

That said, it’s unlikely Chinese equities will lead the way alone, and we think the winners and losers may change depending on how quickly and effectively a vaccine can be rolled out. We’d expect opportunities to arise for some undervalued names.

On the fixed income side, we’ll have to be more selective. A combination of low term premiums in contrast with continued easy monetary policy maintains a challenging environment for fixed income investors. But, emerging market fundamentals, especially within Asia, have improved in recent months as foreign demand offsets continued domestic weakness in certain economies. In our view, emerging market local currency bonds could become more attractive.

Bonds Have More Room to Run

Desmond Soon

One might consider 2020 to be the year of the poisoned rat, but as we enter the year of the ox, we have reasons to think we’ll see a stronger year marked by hard work. We generally have strong convictions on Asian currencies and local currency bonds. While flows into Asia dollar bonds had taken off significantly throughout last year, local fixed income bonds and equities have lagged, and we think they have room to catch up.

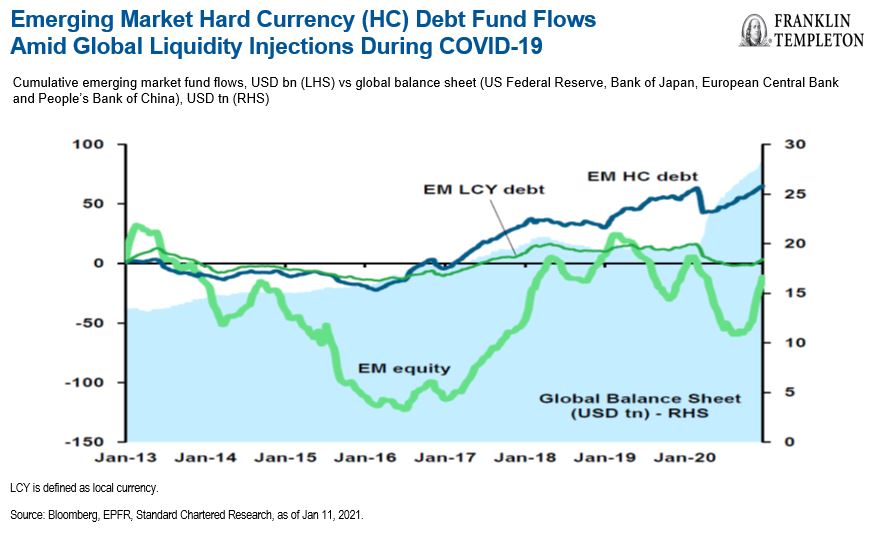

A number of Asian economies are net-creditor nations, those that invest more in other countries than others invest in them. As major Western economies monetize their debt to support their economies from the financial effects of the global pandemic, local Asian economies and their currencies will likely be a sweet spot for 2021—particularly currencies that are linked to countries with strong export growth, in our view. Container prices have surged, particularly in Chinese ports—which illustrates this strength in exports. While pandemic-induced supply bottlenecks have played a role, this growth is due to overwhelming demand. Despite the encouraging evidence, we believe emerging market local currency debt remains underappreciated by investors, as seen in the chart below.

Emerging market investors should be aware of the bipolarization of the investment landscape. China is not your average emerging market—it is the second-largest economy in the world.

The sheer size of the Chinese bond market has led to demand for dedicated Chinese bond funds to provide market access for foreign investors to trade, settle and hold bonds tradable on the China Interbank Bond Market and Bond Connect (HK). However, given what happened in the United States under former President Trump, who sanctioned a list of Chinese companies, some investors remain hesitant on emerging market global indexes and prefer to consider China as a separate allocation within an emerging market portfolio. That said, Chinese bonds offer strong yield pickup for investors; the 10-year Chinese government bond today yields more than 3%, compared to the 10-year US Treasury at just over 1%.

Fertile Ground for Patient Stockpickers

Michael Lai

As market expectations for a sharp rebound continue, geopolitics present an ongoing headwind for business investment decisions. In the United States, Joe Biden’s presidency seems to have calmed financial markets as investors enjoy much-needed clarity on many issues, along with the easing of US-China tensions. We saw a bit of a rebound in markets in January when Biden announced that he is open to “meeting China halfway,” with the general realization that China is a major strategic rival.

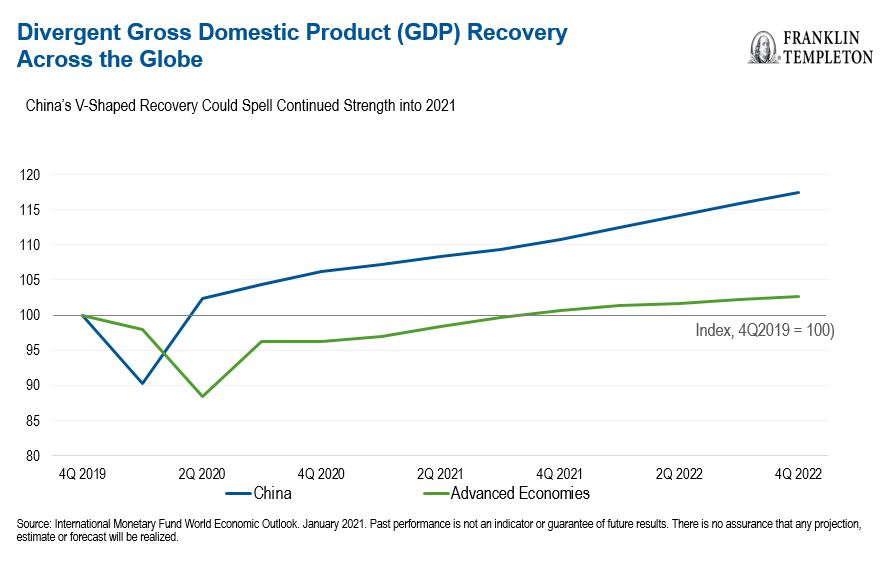

In our view, China has handled the pandemic very well, and the strength of its economic recovery is unparalleled. The skill and speed at which authorities dealt with the pandemic resulted in a V-shaped recovery that we believe bodes well for continued strength in the year ahead. Chinese economic policy will likely focus on normalization throughout 2021, through monetary, fiscal or regulatory policy.

In my 30 years of experience as a stockpicker, I’ve been amazed at the opportunities the Chinese equity market has presented to investors—the depth and breadth of the market has grown exponentially. China is relatively unique in that although it does not follow a liberal, market-oriented Western policy script, it nonetheless offers investors a diverse opportunity set.

Digitization, adoption of technology and further consolidation across certain industries should all feed into the long-term opportunities that we’ve long been watching unfold in China. More recently, the government’s commitment to achieving a carbon-neutral footprint within the next decade could throw up some interesting opportunities in the renewables space, as well as the new energy and electric vehicles sector.

We’re particularly interested in so-called “new economy” stocks. The trajectory of companies that have harnessed technology to create online platforms from traditional brick-and-mortar businesses has ticked off some Chinese government initiatives—from lower transaction costs to reaching segments of society that previously did not have that access to goods and services. Looking ahead, the concept of digitization extends beyond the consumer section in terms of how we consider fifth-generation (5G) technology, as we think it could become a tailwind for other sectors to capture this opportunity, particularly in the industrials sector.

While the ox can be stubborn, as we head into the new year, we’ll take a healthy dose of the ox’s most well-known quality: patience. As we continue to keep an eye on quality businesses with sustainable business models, we also anticipate ongoing Chinese initiatives that could bring fertile investment opportunities.

For timely investing tidbits, follow us on Twitter @FTI_emerging and on LinkedIn.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size and lesser liquidity. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton’s U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Related Articles

Emerging Markets Eclipse Developed Markets

The evidence of stronger emerging market fundamentals is indisputable. Here are some of the main reasons why emerging markets are

Direction of developing economies uncertain

The credit crisis plaguing much of the developed world is also leaving its mark on developing economies. With the global financial

Shifting Climate, Shifting Opportunities

Climate change—like any type of disruption—has disparate impacts on people, places and things. It can also have disparate impacts on