As we travel around the world meeting business leaders and investors, we’ve cemented our view that emerging markets equity today is a very different asset class from when we started our careers some 25 years ago.

There are few better illustrations of that evolution than the central role innovation and the use of technology now play in emerging markets. But it’s clear from our research that understanding of the potential opportunity in these areas continues to elude many investors.

We see a huge amount of innovation and proprietary knowledge coming through from emerging markets.

While many investors expect emerging markets to follow the development path of more advanced markets, in reality we are witnessing companies seize the lead in innovation and leapfrog the more advanced economies in areas such as e-commerce, digital payments, mobile banking and electric vehicles. Innovative companies are turning previous structural weaknesses into strengths.

Unhindered by sunk investments in legacy systems or infrastructure, they have ample room to come up with forward-thinking and profitable solutions.

The most high-profile example is China, where companies have developed from a replication and simulation approach to leading with their own proprietary research and development (R&D) spend to differentiate themselves from Western products.

A new generation of affluent and savvy Chinese consumers, faced with a lack of retail stores and malls, began turning to their smartphones to purchase goods online. Today, e-commerce makes up a far higher percentage of retail sales in China than in the United States.

A similar trajectory can be seen in digital payments, where the slow development of credit card systems has prompted a consumer migration to online payment platforms such as Alibaba’s Alipay and Tencent’s WeChat Pay.

Alipay, for example, had a total third-party payment market share of 50% in December 2018 (total payment volume), while WeChat Pay also held a 35% share—with the latter expected to reach 40% market share by the end of 2019.1 Digital payments have now become commonplace across China, and the value of its digital payment market is multiple times that of the United States.

Made in China: Outdated Stereotypes of Emerging Market Exports Remain

Despite emerging market product advancements in many areas, a recent survey carried out on behalf of Franklin Templeton’s Emerging Market Equity Group suggested UK investors remain hesitant about the value and quality of some emerging markets exports, with many holding outdated stereotypes of products and services “Made in China.”

More than half of investors surveyed considered Chinese exports to be “cheap” (53%), with some also describing them as “poorly regulated” (38%) and “low quality” (29%). 2By comparison, most respondents described UK exports as “well-regulated” (62%) and “reliable” (57%), whilst Japanese products were considered to be both “high quality” (58%) and “innovative” (52%).3

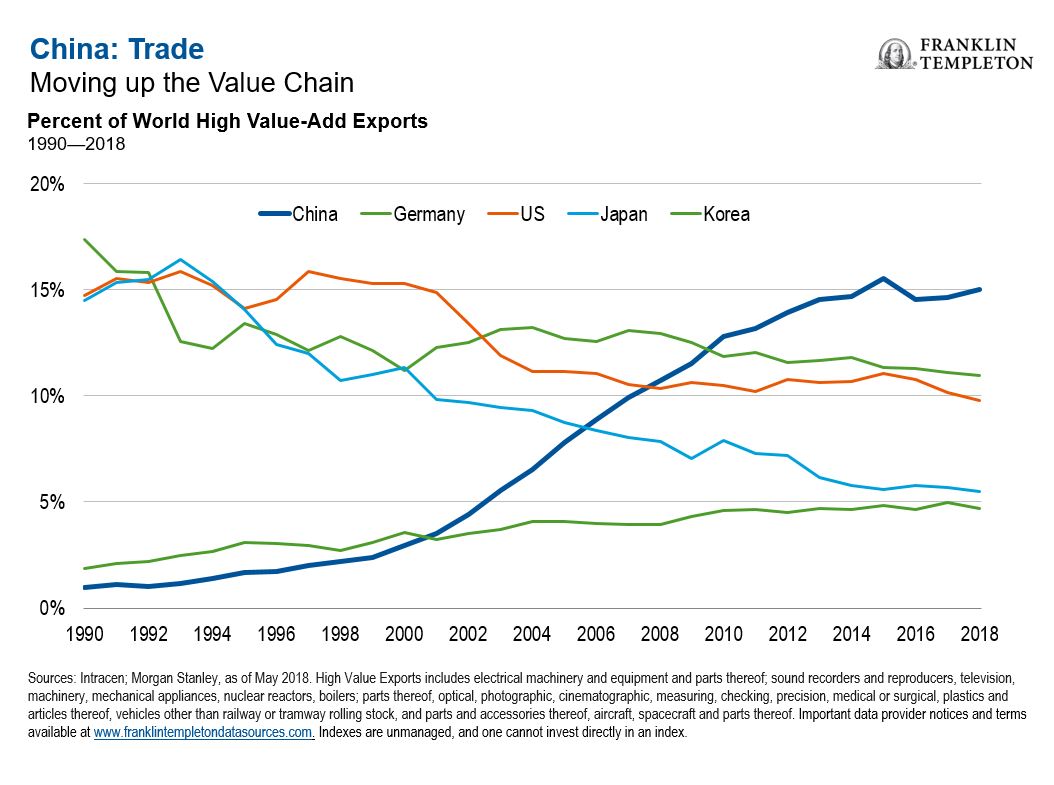

Where once emerging markets economies achieved initial success as producers of cheap home appliances or electronic parts, for example, many of these economies have now set their sights further up the value chain. Indeed, with China and South Korea as leading examples, emerging markets’ share of global high value-add exports has risen dramatically since the start of the 21st century, rendering this impression of survey participants out of step with reality.

Of course, progress is uneven across emerging markets and we should not downplay the challenges that certain countries still face in their development. This is where we believe on-the-ground research and an active investment approach become critical.

We think some of the most disruptive innovations have hailed from emerging economies, and we expect them to continue to leap ahead in an increasing number of areas. Certain companies have shown exceptional agility in solving consumers’ problems, and those that can continue to do so are likely to enjoy sustainable earnings growth.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

The comments, opinions and analyses expressed herein are solely the views of the author(s), are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FT affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

_________________________________

1. Source: HSBC as of December 2018. There is no assurance that any estimate, forecast or projection will be realized.

2. Research conducted on behalf of TEMIT by Cicero Group. All figures, unless otherwise stated, are from Cicero Group. Total sample size was 2,270 UK consumers (18+), with 1,379 UK investors who invest of which 1,032 hold investments of at least £25,000. 505 of the total sample are 18–34 and are current or future investors. Fieldwork was undertaken between 18th–26th February 2019. The survey was carried out online.

3. Ibid.