Three Reasons We Remain Bullish on Emerging Markets Long Term

Emerging markets have seen progress on back of an uptick in vaccination rollouts, but the recent Chinese regulatory crackdown and further virus outbreaks have caused equities to generally underperform year to date relative to developed markets. With a focus on emerging markets outside of Asia, our Emerging Markets Equity Senior Managing Director Chetan Sehgal nonetheless remains bullish on the long-term potential of emerging markets and outlines three main reasons: debt, valuations and cashflows.

THREE S’S: FRANKLIN TEMPLETON EMERGING MARKETS EQUITY’S INVESTMENT PILLARS

We take a long-term, fundamental, bottom-up investment approach with a focus on three main pillars.

1. Structural opportunities, which we call the beta within the asset class. We seek to capitalize on long-term structural trends such as demographics, technology, and consumption, and this is the lens through which we look when assessing the outlook for emerging market countries.

2. What we look for within these structural opportunities represents the second pillar, sustainable earnings power. We seek to buy shares of companies with long-term earnings potential at a discount to their intrinsic worth.

3. Stewardship is the delta, which represents the difference we try to make as investors through our relationships and engagement with companies to promote positive change.

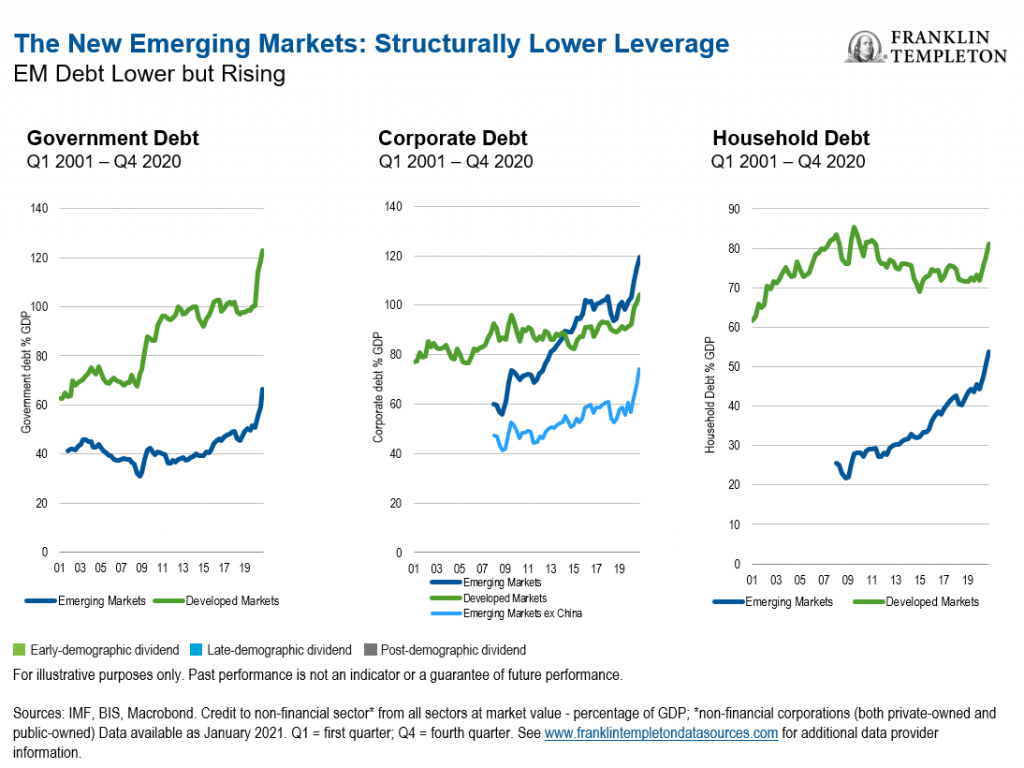

Emerging Market Debt Remains Relatively Low

As we examine the emerging markets landscape today, the rise of leverage within economies is a key trend we have witnessed. Leverage can be a double-edged sword, as it can be positive, but also represents a source of risk. Over the past decade, the level of debt has gone up not just in emerging markets, but across the world. COVID-19 has certainly led to a dramatic increase in government debt in some countries, but in general, debt to gross domestic product (GDP) is currently much lower in emerging economies than in developed countries—which is one reason for our bullish view.

Aside from an increase in China, corporate debt as well as household (consumer) debt levels in emerging markets are still much lower than in the developed world, too. As such, we feel that emerging markets have much more headroom available to further increase debt levels without a significantly detrimental impact.

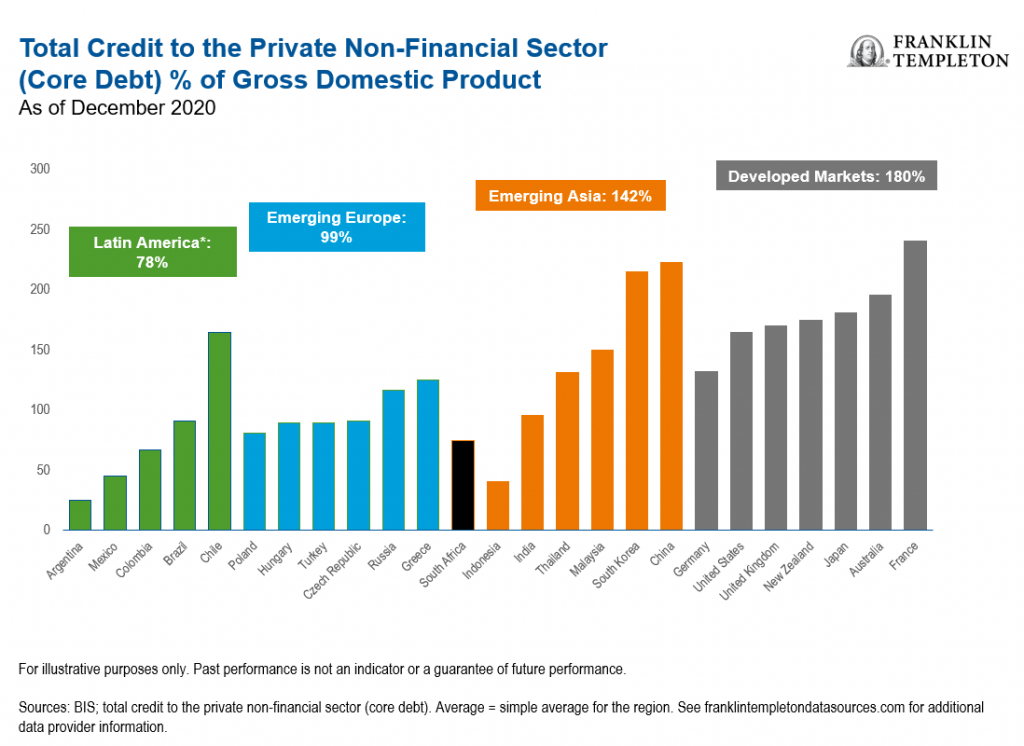

Turning to the structural opportunity this presents, the credit ratios in Latin America and emerging Europe are much lower as a percentage of GDP compared with both the developed world and emerging Asia. This is the reason Latin America and emerging Europe have looked appealing to many investors despite some headwinds. Mexico for example, boasts a debt-to-GDP ratio of less than 50% and while Brazil’s debt-to-GDP is around 100%, it is still much lower than many developed countries.1 We see a similar story in Eastern Europe, where debt levels are lower in Turkey, Hungary and Poland than countries like Japan, Australia, France, for example, where debt-to-GDP ratios are above 150%.2

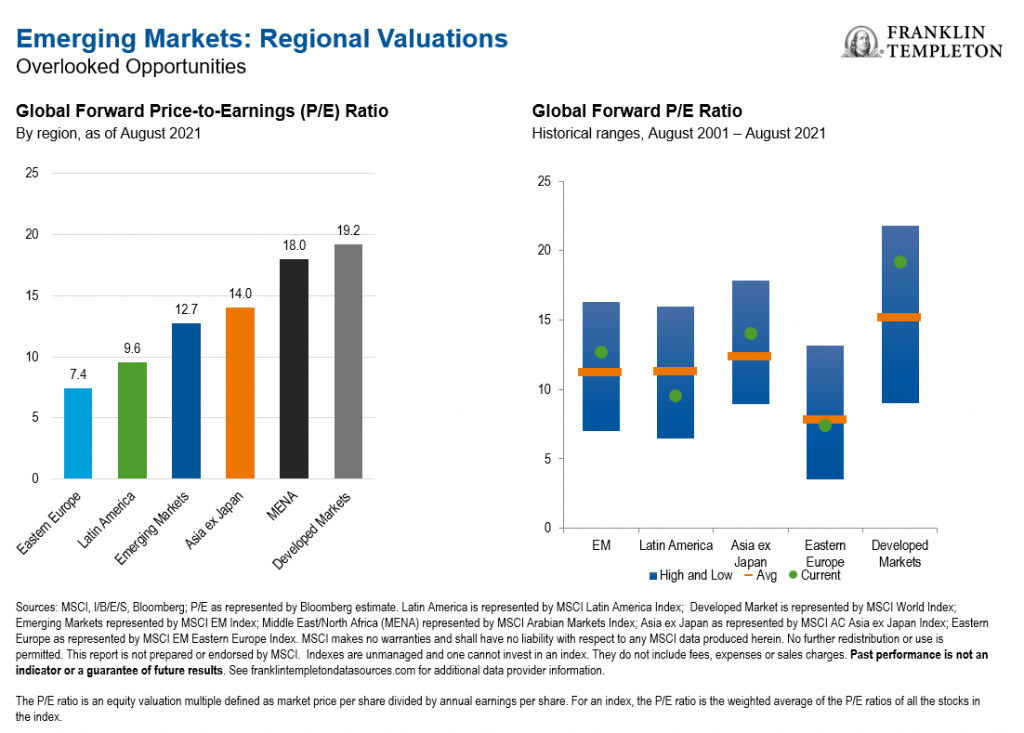

Attractive Valuations—particularly in Latin America and Eastern Europe

Emerging market equities also hold attractive valuations—another reason for our bullish view. They trade at a discount to the developed world despite strong growth potential and headroom for credit consumption. The forward price-to-earnings (P/E) ratio for emerging markets, as measured by the MSCI Emerging Markets Index, stands at around 13, whereas developed stocks, as represented by the MSCI World Index, have a forward P/E ratio of around 19.3

Valuations in Eastern Europe and Latin America are even lower—and not just on an absolute basis, but even relative to their own history. Latin America is rich in natural resources and looks to benefit from the commodity boom taking place amid the recovery from the pandemic. The prices of most of commodities have risen, which represents a natural tailwind for the economies in those regions, with improving terms of trade being one benefit. Brazil is one of the world’s leaders in iron ore production, for example. And Brazil—along with Argentina and Chile—also supply the world with lithium, one of the most important metals in electric vehicle production. Chile and Peru are global leaders in the production of copper, another vital commodity in today’s world that has seen increased demand.

Similarly, countries in Eastern Europe—primarily Russia—are key commodity producers, including nickel, aluminum and of course, Russia is a leading oil-producing nation. Much of the world depends on the commodities produced in Latin America and Eastern Europe, which should bode well for these economies and the companies within related industries.

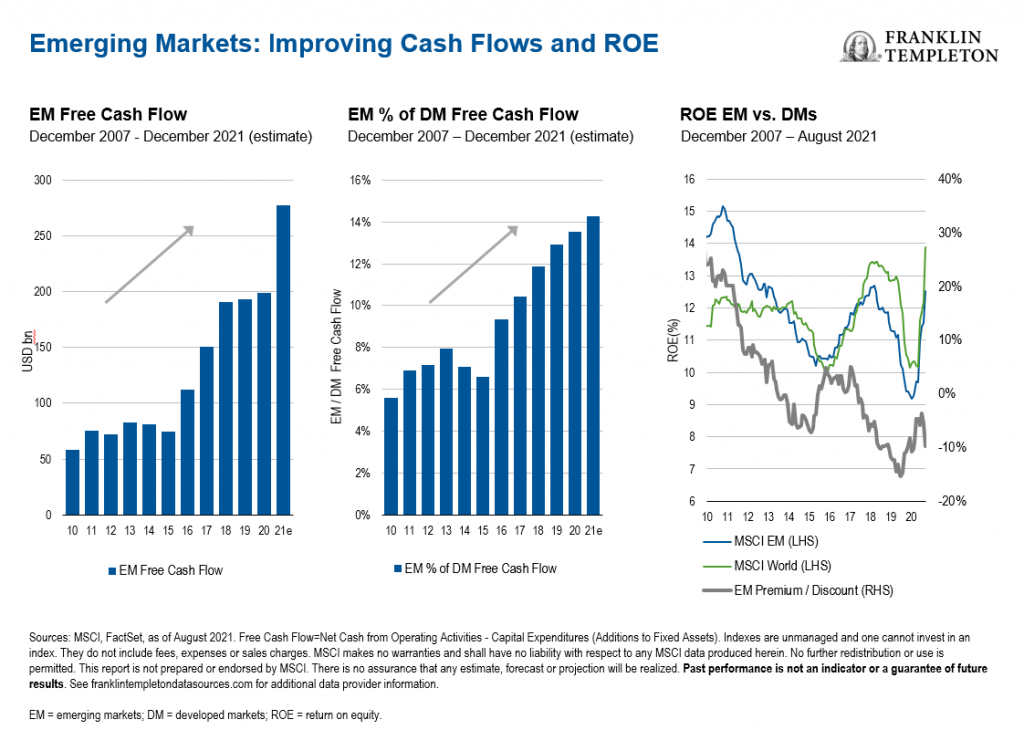

Improving Cashflows

Cashflows are another reason why we like emerging markets. In the last decade, emerging markets have underperformed the developed world in terms of return on equity. But for the last decade there has been a trend of improving free cash flows (in both absolute terms and relative to developed markets) that has accelerated in the last year. Emerging market companies are generating much more free cash this year because both commodity-oriented and technology-oriented companies (in particular the semiconductor industry) have been doing well. As cashflows increase, we believe ultimately this will result in improved returns on equity for emerging market stocks and should likely propel a rerating.

While we do see reasons to be optimistic, we should mention the near-term risks in our outlook. Regulatory changes happening in China have ramifications for a number of industries and many internet related stocks in particular. This is impacting earnings power in the near term, and also potentially further into the future.

And of course, we are still living with COVID-19 and the more infectious variants. We had expected with rising vaccination rates, mobility would automatically resume. However, that hasn’t necessarily been the case. In Singapore, for example, the vaccination rate is now above 80%, but COVID-19 cases remain widespread, and many mobility restrictions are still in place.

We would also note that while commodity prices have been very strong this year, they seem to be topping because of China’s policy measures as well as the global resurgence of COVID that has acted to suppress demand during lockdown periods. In addition, a dramatic rise in freight rates has had a negative impact on margins for many export-oriented companies.

In sum, we believe the long-term fundamentals for emerging markets remain attractive despite near term headwinds, and that equities offer good potential for investors. While the economic recovery from COVID-19 could be more muted going forward, growth remains historically strong, valuations appear cheap, and earnings prospects are supported by rising cashflows.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

There is no assurance any estimate, forecast or projection will be realized.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

____________________________

1. Source: Bank of International Settlements (BIS), as of December 2020.

2. Source: Ibid.

3. Source: The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

Related Articles

The Answer Is Blowing in Brazil’s Wind

Renewable energy production in Latin America has grown dramatically over the last decade. The use of green technology like wind

All emerging market bonds are not the same

Emerging market debt is relatively safe and offer potentially greater yields As emerging market (EM) bonds become an increasing larger

The time to invest in emerging markets is now

Despite recent outflows, the fundamental case for long-term investing in emerging-market equities remains well-founded. · Not all emerging-market companies are